Why ocean finance needs rules before it needs applause

A recent article in the TIME Oceans Issue made me pause.

Justin Worland’s piece, Oceans of Value, describes a fast-growing world of companies, investors, and entrepreneurs looking at the ocean not only as a place in trouble, but as a new field of opportunity. Seaweed packaging. Microplastic filters. Ocean thermal energy. Coral-reef replicas. Blue bonds. Debt-for-nature swaps. A whole language is emerging around ocean innovation, ocean investment, and the “blue economy.”

At first glance, this sounds hopeful. The ocean is under pressure from almost every side: overfishing, pollution, climate change, warming seas, coastal development, biodiversity loss, and the decline of coral reefs. Governments and non-profits alone are not funding the scale of protection and transition needed. So yes, finance matters. Serious money can help.

But the TIME article also points to the uncomfortable question underneath all this excitement:

If the ocean becomes an investment category, who decides what counts as sustainable?

That question matters.

Because money does not become ethical because it is painted blue.

The ocean needs finance. But not just any finance.

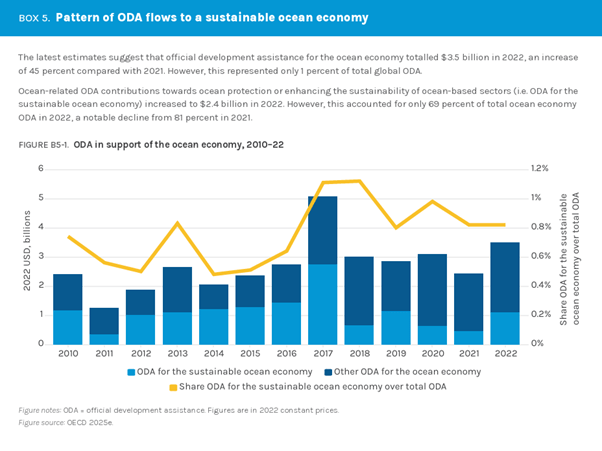

The Ocean Panel estimates that current investment falls far short of what is needed for long-term ocean health. It points to an estimated need of around 550 billion US dollars annually to secure a sustainable ocean economy, while less than 1% of official development assistance and philanthropic funding currently goes to ocean sustainability.

That gap is real.

There is no credible ocean protection strategy that pretends finance does not matter. Marine protected areas need management. Wastewater systems need infrastructure. Fisheries need monitoring and enforcement. Coastal communities need resilience. Reef restoration, where appropriate, needs long-term science and follow-up. Small island and coastal states need access to capital on fair terms.

Blue finance can help with that.

But finance is not the same thing as protection.

A project can attract capital and still harm the ecosystem it claims to support. A coastal development can use the language of “nature-positive tourism” while increasing wastewater, reef pressure, boat traffic, anchoring damage, or coastal exclusion. A coral restoration project can produce beautiful images while failing to reduce the stressors that caused reef decline in the first place. A blue bond can sound impressive while leaving ordinary people unclear about what is actually protected, who benefits, who monitors, and what happens when targets are missed.

That is why the question is not simply: can the ocean attract investment?

The better question is: can finance accept ocean rules?

What “blue economy” should mean

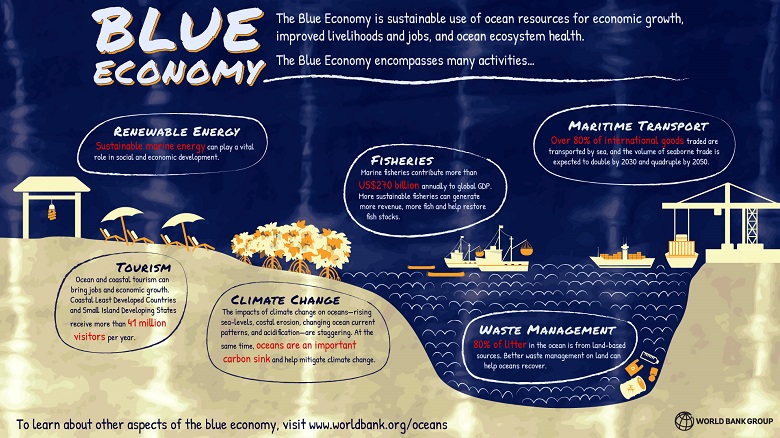

The World Bank’s definition is useful because it keeps the tension visible. The blue economy is not just economic activity related to the sea. It is the sustainable use of ocean resources for economic growth, improved livelihoods, and jobs while preserving ocean ecosystem health.

That last part is not decorative. It is the test.

If ocean-based economic growth does not preserve ecosystem health, it is not truly blue. It is just ocean extraction with better branding.

For divers, this matters directly. The dive industry is part of the blue economy. Dive resorts, liveaboards, training centres, underwater photography, marine tourism, reef restoration projects, citizen science, and conservation claims all sit inside this wider ocean economy.

That means we should not only ask whether a dive destination is beautiful, affordable, or well marketed. We should also ask:

Does tourism stay within reef carrying capacity?

Is wastewater treated properly?

Are boats moored safely?

Are reefs monitored over time?

Are local communities benefiting?

Are marine protected areas real, or only lines on a map?

Are restoration claims backed by science, survival data, and protection of the wider ecosystem?

A reef does not care how good the brochure looks.

The principles already exist

This is not about inventing impossible moral purity tests. Several serious frameworks already exist.

UNEP FI’s Sustainable Blue Economy Finance Principles provide a practical starting point for banks, insurers, and investors. They call for finance that is protective, legally compliant, risk-aware, systemic, inclusive, transparent, purposeful, precautionary, partnering, and science-led.

That language may sound institutional, but underneath it is a simple idea:

Do not finance ocean projects that undermine the ocean systems they depend on.

UNEP FI’s Turning the Tide guidance goes further by helping financial institutions distinguish between ocean activities to support, activities to challenge, and activities to avoid because of their damaging nature.

That last category matters.

Not everything should be improved, compensated, or rebranded. Some activities should simply be out.

For me, that is one of the most important lessons in the blue economy debate. A serious ocean-finance approach needs opportunity, yes. But it also needs exclusion. Red lines. No-go zones. Activities that are too destructive, too risky, or too dishonest to be financed under a blue label.

Blue bonds and debt-for-nature swaps: promise, but not magic

The World Bank and IMF examples show why this debate is not theoretical.

The Seychelles blue bond is often cited as a landmark case. It raised finance for marine conservation and sustainable fisheries, and complemented wider marine protection efforts. Belize’s debt-for-nature swap is another important example. The IMF describes how Belize used a debt transaction to reduce external debt and generate long-term funding for marine conservation, with commitments to expand marine protection and support conservation financing over time.

These examples are promising because they link finance to real commitments: protected areas, conservation funds, fisheries governance, marine spatial planning, and long-term funding mechanisms.

But they also show why the receipt must be checked.

The announcement is not the outcome. The bond is not the protection. The financial structure is not the reef.

The real questions come after the headline:

What is legally committed?

Who monitors progress?

Are there penalties if milestones are missed?

Is there a conservation fund?

Who sits on its board?

Are local actors involved?

Is the money actually reaching protection, enforcement, restoration, resilience, or livelihoods?

What happens after the first funding cycle ends?

This is where blue finance becomes serious — or becomes bluewashing.

The danger of the beautiful claim

One of the reasons I am interested in this topic is that divers live close to the gap between claim and reality.

We see the reef, not just the report. We see whether boats anchor badly. We see whether divers are briefed properly. We see whether coral gardens are healthy or neglected. We see whether dive operators treat marine life as scenery, a commodity, or a living system.

And we also see how easily beautiful ocean language can hide weak practice.

“Eco.”

“Regenerative.”

“Nature-positive.”

“Blue.”

“Reef-friendly.”

“Conservation-based.”

None of these words are proof.

The proof is in the system around the claim.

A good blue-finance project should be able to show what it protects, what it changes, who benefits, who carries the risk, and how results are measured over time. A good reef-restoration project should be able to explain not only how coral is planted, but how the reef is protected from the pressures that damaged it. A good tourism project should be able to talk honestly about limits: wastewater, carrying capacity, access, boat traffic, local benefit, and governance.

If a claim cannot survive those questions, it is not yet a blue claim.

It is marketing.

A diver’s way to read blue finance

Maybe this is where diving offers a useful metaphor.

Before entering the water, we do not just admire the surface. We check the site conditions. We check our equipment. We plan our gas. We agree on limits. We identify hazards. We know when to call the dive.

Blue finance needs the same discipline.

Before entering the ocean with capital, investors should check the conditions:

Is the project protective?

Is it science-led?

Is it legally compliant?

Is it transparent?

Is it inclusive?

Is it risk-aware?

Is it accountable over time?

Does it have red lines against harm?

If not, call the dive.

That may sound severe. But the ocean is not a neutral investment space. It is a living commons. It regulates climate, feeds people, protects coasts, carries cultures, supports livelihoods, and holds forms of life we still barely understand.

Treating it as an asset class without treating it as a living system is dangerous.

Blue money is only useful if it serves the ocean

The TIME article is right to identify a new wave of ocean investment. There are real opportunities here. Seaweed alternatives to plastic, microplastic filters, better fisheries finance, marine protection, coastal resilience, offshore renewable energy, and well-designed conservation finance can all contribute to a more serious ocean transition.

But the excitement should not come before the rules.

The ocean does not need more beautiful claims. It needs limits, proof, monitoring, community benefit, and accountability. It needs public governance, science-based standards, and financial institutions willing to say no when an activity is harmful enough to be excluded.

So I come back to the same simple test:

Blue money is only useful when it serves living ocean systems.

Not the other way around.

Sources and further reading

TIME Oceans Issue — Justin Worland, “Oceans of Value”

Ocean Panel — “Ocean Finance for the Sustainable Ocean Economy”

UNEP FI — Sustainable Blue Economy Finance Principles

UNEP FI — “Turning the Tide: How to Finance a Sustainable Ocean Recovery”

World Bank — Blue Economy and Seychelles blue bond materials

IMF — Belize debt-for-nature swap and debt-for-nature swap analysis

Leave a comment